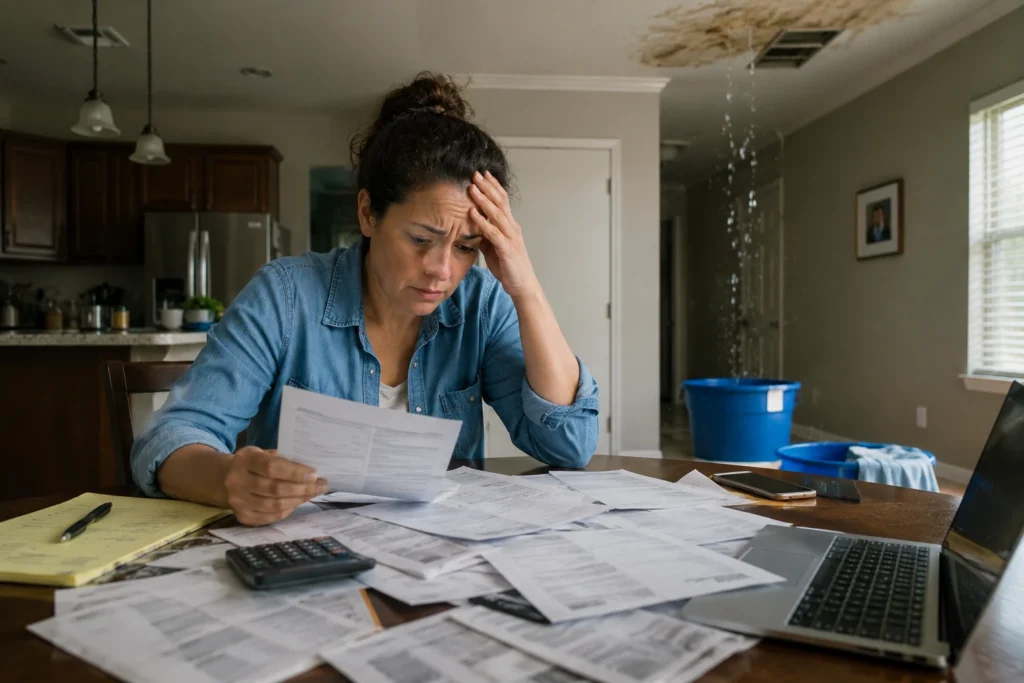

Hailstorms in South Texas create chaos fast. One afternoon the roof looks perfectly fine. A few hours later, homeowners are taking photos of shingles in the yard, water stains spreading across ceilings, dented gutters, cracked vents, and damaged siding. Then the insurance process begins. And honestly? That is where confusion often gets worse. When people search for Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX, they are usually trying to answer one big question:

Who is actually protecting my interests during this claim? That question matters more than most homeowners realize. I have seen situations where storm damage claims move smoothly from inspection to payment. I have also seen claims become exhausting battles involving delays, low estimates, missing damage, policy disputes, and repeated inspections. The difference often comes down to documentation, negotiation strategy, and understanding who each adjuster actually works for.

This is not just about roofs. It is about money, leverage, evidence, and long-term property protection. And in a place like Laredo, where severe weather can hit hard and roofing systems absorb brutal heat year-round, the stakes become even higher. Let’s break it all down clearly.

Why Hail Claims in South Texas Become Complicated Fast

Hail claims sound simple on paper. A storm damages the roof. Insurance pays for repairs. Problem solved. Reality rarely works that smoothly.

Hail Damage Is Not Always Obvious

Some hail damage screams for attention immediately. Missing shingles. Broken skylights. Bent flashing. Easy to spot. Other damage hides quietly for months.

Granule loss on asphalt shingles may not leak immediately but can shorten roof lifespan significantly. Metal panels may appear “cosmetic” while protective coatings have actually been compromised. Vent caps, ridge systems, flashing components, and soft metals often reveal the true severity of the storm before the shingles do. That is where many disagreements begin. A homeowner sees real damage. The carrier sees “minimal impact.” Huge difference.

Laredo Weather Creates Unique Challenges

South Texas weather is rough on roofing systems even before hail arrives. Extreme heat. UV exposure. Rapid expansion and contraction. Then hailstorms enter the picture and accelerate existing weaknesses dramatically.

In Laredo, timing matters too. A roof inspected weeks or months after the storm may already show signs of weathering that complicate the claim investigation. Insurance companies may argue deterioration occurred naturally instead of during the hail event. This is why documentation becomes critical immediately after a storm. Photos matter. Weather reports matter. Inspection timing matters. Everything matters.

Why Homeowners Feel Overwhelmed

Most property owners are not insurance experts. Nor should they be.

But suddenly they are expected to understand:

- Deductibles

- Scope sheets

- Depreciation

- Coverage exclusions

- Supplemental estimates

- Replacement cost calculations

That is a lot to absorb while dealing with roof leaks and contractor calls. And unfortunately, confusion creates mistakes. Some homeowners accept low offers too quickly. Others delay inspections so long that evidence weakens. Some trust verbal promises that never appear in writing. The process becomes stressful fast.

What an Insurance Adjuster Actually Does

Let’s start here because many people misunderstand this role completely. An insurance adjuster is not automatically your enemy. But they are not your personal advocate either. That distinction matters.

Who the Insurance Adjuster Works For

Insurance adjusters represent the insurance company. Their responsibility is to evaluate the claim based on policy language, inspection findings, and company procedures.

There are usually two main types:

| Type | Description |

| Staff Adjuster | Direct employee of the insurance carrier |

| Independent Adjuster | Third-party contractor hired by the insurer |

Both ultimately work on behalf of the carrier. That does not automatically mean bad faith. Many adjusters are experienced professionals trying to handle claims fairly. But their role is tied to the insurance company’s interpretation of the loss. Not the homeowner’s.

The Typical Insurance Claim Process

Most hail claims follow a similar pattern:

- Claim is reported

- Inspection gets scheduled

- Property is evaluated

- Damage scope is created

- Coverage decision is issued

- Settlement offer is made

Simple in theory. Complicated in practice.

The inspection itself may last under an hour. Yet that short visit heavily influences thousands sometimes tens of thousands of dollars in repair costs. That creates pressure.

Strengths of Insurance Adjusters

To be fair, insurance adjusters do provide important value. On straightforward claims, they can move the process quickly. Many handle storm claims efficiently and professionally. When damage is obvious and undisputed, homeowners may receive fair settlements without major problems.

Advantages can include:

- Faster claim handling

- Standardized estimating software

- Structured procedures

- Familiarity with policy terms

- Quick payment issuance on clear claims

Some hail claims truly are simple.

Others are not.

Common Limitations Homeowners Encounter

This is where frustration often begins. After major storms, adjusters may handle huge claim volumes. Time becomes limited. Inspections become rushed. Some damage gets overlooked entirely.

Common homeowner complaints include:

- Missing roof accessories

- Undervalued materials

- Omitted flashing components

- Ventilation exclusions

- Low labor pricing

And here is something many property owners do not realize: The field adjuster inspecting the property may not even control the final payment decision. Desk reviewers, supervisors, and internal claim departments often influence settlement outcomes later. That can create disconnects between what was discussed onsite and what eventually appears in the estimate.

What a Public Adjuster Does for Homeowners

Now let’s look at the other side of the equation. A public adjuster works for the policyholder. Not the carrier. That changes everything about the claim strategy.

Public Adjusters Represent the Insured

A licensed public adjuster advocates for the homeowner or property owner during the insurance claim process.

Their goal is to:

- Evaluate damage independently

- Review the insurance policy

- Document losses thoroughly

- Negotiate for covered compensation

This is the core difference in the Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX discussion. One represents the carrier. One represents the insured. Completely different alignment.

Services a Public Adjuster Typically Provides

A strong public adjuster usually handles far more than simple negotiations.

Services may include:

- Detailed property inspections

- Roof damage analysis

- Policy interpretation

- Scope preparation

- Supplemental estimate creation

- Claim communication management

- Evidence organization

- Carrier negotiation

Good documentation changes claims dramatically. I cannot overstate that enough.

Why Public Adjusters Are Common in Large Hail Claims

Complex claims create complexity for everyone involved. Commercial properties. Large homes. Metal roofing systems. Multi-structure properties. These losses often involve thousands of individual estimate line items. That is where experienced claim representation becomes valuable.

Especially when disputes arise regarding:

- Functional damage

- Code upgrades

- Matching issues

- Overlooked components

- Interior water intrusion

- Supplemental repairs

When Homeowners Usually Hire One

Many homeowners initially try handling claims alone. Sometimes that works perfectly fine.

But public adjusters are often brought in when problems appear, including:

- Denied claims

- Delayed claims

- Underpaid estimates

- Multiple reinspections

- Conflicting contractor opinions

- Communication breakdowns

At that point, frustration is usually already high.

Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX

Now let’s compare them directly.

| Category | Insurance Adjuster | Public Adjuster |

| Represents | Insurance company | Policyholder |

| Goal | Evaluate claim for carrier | Maximize covered settlement |

| Payment Source | Insurance company | Percentage of claim recovery |

| Policy Interpretation | Carrier-focused | Insured-focused |

| Negotiation Role | Carrier representative | Homeowner advocate |

| Documentation Depth | Varies by workload | Typically extensive |

| Supplemental Claims | Often reviewed internally | Aggressively pursued |

| Communication Priority | Carrier procedures | Policyholder interests |

This table explains why the phrase Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX matters so much during storm recovery. The incentives are different. The priorities are different. The approach is different.

The Biggest Difference: Loyalty

This is the heart of the discussion. Insurance adjusters work for insurance carriers. Public adjusters work for homeowners. That does not automatically mean one is good and the other is bad. But it absolutely affects how claims are approached. And experienced property owners understand this quickly.

Communication Changes Everything

One of the biggest advantages strong public adjusters bring is organization.

Claims often improve when communication becomes:

- Structured

- Evidence-based

- Consistent

- Professional

Emotional arguments rarely move claims forward. Documentation does.

Common Problems Homeowners Face During Hail Claims

Storm claims create recurring patterns. I see the same issues repeatedly.

Underpaid Roof Damage Estimates

This happens constantly.

The initial estimate may exclude:

- Flashing

- Ridge caps

- Starter shingles

- Gutters

- Vent systems

- Drip edge

- Underlayment

Small omissions add up fast. Especially on larger roofs.

Cosmetic vs Functional Damage Disputes

This is one of the most frustrating areas in hail claims. Insurance carriers sometimes argue the damage is “cosmetic only.” But cosmetic appearance is not always the full story. Functional concerns matter too. Granule displacement can shorten shingle lifespan. Protective finishes on metal surfaces may become compromised. Flashing deformation may affect waterproofing over time. Those details become central in the Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX debate because interpretation often determines payout value.

Delays and Reinspections

Some claims drag on for months.

Reasons may include:

- Rotating adjusters

- Supplemental disputes

- Internal reviews

- Engineering inspections

- Contractor disagreements

The longer claims stretch out, the more stressful they become. Especially when repairs cannot begin.

Denied Claims Despite Visible Damage

This shocks homeowners. Visible damage exists. Yet the claim gets denied.

Common carrier arguments include:

- Wear and tear

- Mechanical damage

- Old storm damage

- Lack of storm correlation

- Improper maintenance

At that stage, documentation becomes absolutely critical.

How Public Adjusters Help Strengthen Hail Claims

Good public adjusters do more than argue. They build evidence. That distinction matters enormously.

Better Documentation

Strong claims rely on organized proof.

That may include:

- Wide-angle roof photos

- Close-up impact images

- Weather data

- Moisture readings

- Contractor evaluations

- Timeline records

The goal is not emotion. The goal is credibility.

Understanding Policy Language

Insurance policies are full of technical wording most homeowners rarely read until disaster strikes.

A public adjuster may help interpret:

- Deductibles

- Exclusions

- Coverage limitations

- Matching provisions

- Ordinance and law coverage

That interpretation can significantly affect settlement outcomes.

Supplemental Negotiation Experience

This is huge in hail claims. Initial estimates are often incomplete. Supplemental negotiations address missed items or additional repair costs discovered later. Experienced adjusters understand estimating systems like Xactimate and know how line-item disputes develop during storm claims.

That technical understanding matters. A lot. Many complex storm losses eventually involve supplemental negotiations because the original estimate fails to capture the full scope of repairs. This is especially common with roofing systems where hidden damage appears only after tear-off begins. Homeowners researching Hail Damage Claim Supplements: What Carriers Miss in Their Scope often discover that overlooked items like flashing, underlayment, ventilation components, drip edge, and code-required upgrades can significantly affect the final settlement value. Proper documentation and organized evidence become critical during this stage of the claim.

Reducing Stress for Property Owners

This benefit gets overlooked constantly. Storm claims consume time.

Calls.

Emails.

Inspections.

Paperwork.

Follow-ups.

Many homeowners simply want someone knowledgeable managing the process professionally. And honestly, that alone can provide enormous relief.

Situations Where an Insurance Adjuster Alone May Be Enough

Not every claim requires a public adjuster. That is important to say clearly.

Minor Hail Damage Claims

Small repairs with obvious damage often resolve smoothly.

For example:

- A few damaged shingles

- Minor gutter replacement

- Simple accessory repairs

In these situations, the insurance process may function perfectly well without outside representation.

Fast-Paid Claims With Minimal Complexity

Some claims move quickly because the evidence is clear and the carrier responds appropriately.

No disputes.

No missing scope items.

No negotiation battles.

Excellent. Not every claim becomes adversarial.

Homeowners Comfortable Managing Claims

Some property owners are highly organized and experienced. They document thoroughly. Understand estimates. Review policies carefully. In those cases, managing the process independently may make sense.

Situations Where Hiring a Public Adjuster Makes Sense

Now let’s look at when professional representation becomes more valuable.

Large or Complex Roof Damage

Bigger claims create bigger stakes.

Especially involving:

- Commercial properties

- Multi-family structures

- High-end roofing systems

- Large square footage losses

One overlooked item can mean thousands of dollars.

Denied or Underpaid Claims

This is where public adjusters frequently enter the process. A denied claim is not always the final answer. Sometimes stronger evidence changes everything.

Especially when new documentation reveals:

- Missed impacts

- Code issues

- Hidden damage

- Incomplete inspections

High-Value Properties

Luxury materials complicate estimates quickly. Custom metals. Tile systems. Designer roofing products. Replacement pricing becomes more detailed and disputes become more likely.

Communication Has Broken Down

Repeated delays often signal deeper claim friction. If homeowners feel ignored, overwhelmed, or trapped in endless reinspections, professional advocacy may help stabilize the process. This is one reason the phrase Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX continues gaining attention among frustrated property owners.

Texas Laws Homeowners Should Understand

Texas has important regulations surrounding claims. Understanding them helps avoid serious mistakes.

Public Adjusters Must Be Licensed

Texas requires public adjusters to hold licenses through the Texas Department of Insurance. Always verify credentials before signing agreements. Always.

Contractors Cannot Negotiate Claims

This creates confusion constantly. Roofing contractors can discuss repairs. They cannot legally negotiate insurance settlements on behalf of homeowners in Texas. That role belongs to licensed public adjusters or attorneys.

Understanding Contingency Fees

Most public adjusters work on contingency.

Meaning:

They receive a percentage of the claim recovery.

Fee percentages vary depending on:

- Claim complexity

- Storm severity

- Timing

- Dispute level

Homeowners should review contracts carefully before signing.

Questions Homeowners Should Ask

Before hiring anyone, ask:

- Are you licensed in Texas?

- How much hail claim experience do you have?

- How do you document damage?

- How often will updates be provided?

- Have you handled claims in Laredo specifically?

Specific questions reveal professionalism quickly.

Mistakes Homeowners Should Avoid After a Hailstorm

Some claim mistakes weaken settlements dramatically.

Accepting the First Offer Too Quickly

Initial estimates are not always complete. Review carefully before agreeing. Always.

Waiting Too Long to Document Damage

Evidence fades over time. Weather exposure weakens claim clarity. Early documentation strengthens credibility.

Throwing Away Damaged Materials

Preserve damaged components whenever possible. They may become important evidence later.

Relying Only on Verbal Conversations

Get everything documented. Emails help. Written summaries help. Photos help. Memory alone is unreliable during complex claims.

Hiring Unlicensed Representatives

This creates serious risk. Always verify licensing and reputation before allowing anyone to manage your claim.

How to Choose the Right Public Adjuster in Laredo, TX

Not all representation is equal. Experience matters enormously.

Look for Local Hail Claim Experience

South Texas claims involve unique weather patterns and roofing conditions. Local experience helps.

Ask About Documentation Methods

Strong adjusters rely heavily on evidence. Ask how inspections are performed and documented. Detailed answers matter.

Review Reputation Carefully

Read reviews. Check licensing. Look for consistency. Avoid flashy promises.

Understand the Contract Completely

Never rush into agreements.

Review:

- Fees

- Responsibilities

- Cancellation rights

- Communication expectations

Transparency matters.

Avoid Unrealistic Promises

Nobody can guarantee claim outcomes. Be cautious of anyone promising massive settlements before even inspecting the property. That is a red flag.

Real-World Differences Homeowners Notice During Hail Claim Negotiations

The difference between adjusters becomes most visible once negotiations begin. That is where many homeowners suddenly realize the claim process is not simply about identifying damage. It is about proving scope, justifying pricing, interpreting policy language, and maintaining leverage throughout the discussion.

And honestly, this surprises people. Most homeowners assume visible hail damage automatically leads to a complete settlement. Unfortunately, claim negotiations are often far more technical than expected.

Inspection Depth Can Change the Entire Claim

One adjuster may spend twenty minutes on the property. Another may spend three hours. That difference alone can dramatically affect the outcome.

Thorough inspections often uncover issues such as:

- Detached seal strips

- Soft metal impacts

- Hidden flashing damage

- Ventilation component failures

- Underlayment concerns

- Water intrusion around penetrations

These are not always obvious from ground level. And they are not always included automatically. This is one reason homeowners researching Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX often become frustrated after comparing contractor findings with carrier estimates. The numbers sometimes look wildly different. Not because one side necessarily acted dishonestly. But because inspections vary in depth, urgency, and perspective.

Why Estimates Often Do Not Match Contractor Pricing

This issue creates confusion constantly. A contractor may estimate $35,000 in repairs.

The insurance estimate may show $19,000. Homeowners immediately panic. Who is wrong? The answer is not always simple.

Differences often involve:

| Common Dispute Area | Why It Happens |

| Labor pricing | Market rates fluctuate after storms |

| Code upgrades | Some items require justification |

| Material matching | Carriers may limit replacement scope |

| Overhead and profit | Eligibility disputes occur |

| Tear-off requirements | Building conditions vary |

| Waste calculations | Estimating formulas differ |

This is where experienced negotiation becomes valuable. Not emotional arguing.

Not pressure tactics.

Detailed evidence wins far more often.

The Role of Engineers in Hail Claim Disputes

Some hail claims escalate further and involve engineering inspections. That can intimidate homeowners quickly.

An engineer may evaluate whether damage resulted from:

- Hail impact

- Wear and tear

- Installation defects

- Thermal expansion

- Mechanical damage

- Age-related deterioration

Engineering reports can heavily influence claim direction. And once again, documentation becomes central. Weather reports, inspection photos, prior roof history, maintenance records, and storm timing all matter during these disputes.

Some claim investigations become highly technical and involve concepts similar to phenomenology, where interpretation and observation influence how evidence is evaluated during disputes. In hail claims, small differences in inspection perspective can sometimes lead to dramatically different conclusions regarding roof damage severity and repair scope. Strong claim preparation helps reduce inconsistencies that carriers may later use against the homeowner.

Why Organization Changes Claim Outcomes

I cannot emphasize this enough. The strongest claims are usually the most organized claims. Not the loudest. Not the angriest. Not the most emotional. The most organized.

Homeowners dealing with hail damage should maintain:

- Inspection reports

- Email correspondence

- Claim numbers

- Repair invoices

- Contractor proposals

- Storm-date photos

- Temporary repair receipts

- Timeline notes

This creates credibility. And credibility matters enormously during insurance disputes. Especially when supplemental negotiations begin months later.

Supplemental Claims Are More Common Than Most Homeowners Realize

Many people think the first estimate is final. It often is not. Additional damage frequently appears during repairs, especially involving roofing systems. Contractors may uncover hidden water damage, deteriorated decking, flashing failures, or ventilation issues that were not visible during the original inspection.

That creates supplemental claims. And supplemental negotiations can become one of the most technical stages of the entire process. This is another major reason the topic Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX matters so much. Supplemental handling often separates smooth claims from deeply frustrating ones.

Strong supplements rely on:

- Detailed photo evidence

- Accurate line-item estimates

- Code references

- Clear repair explanations

- Consistent documentation

Without that structure, legitimate damage may still face delays or resistance.

The Emotional Side of Hail Claims Is Real

People rarely talk about this part openly. But they should. Hail claims create stress that extends beyond roofing systems and paperwork. Families worry about finances. Business owners worry about operations. Homeowners worry about leaks spreading during storms.

Then add repeated inspections, delayed responses, and conflicting opinions. It becomes exhausting. This is why experienced claim guidance can provide value beyond settlement numbers alone. Clear communication and organized claim management often reduce enormous amounts of stress during the recovery process. And honestly, that peace of mind matters too.

Final Perspective for Laredo Property Owners

Every hail claim is different. Some move quickly and fairly. Others become complex negotiations involving documentation battles, disputed damage, and supplemental reviews. Understanding the difference between adjuster roles helps homeowners make smarter decisions before problems escalate.

When evaluating Public Adjuster vs. Insurance Adjuster for Hail Claims in Laredo, TX, the key issue is not choosing sides blindly. It is understanding representation, incentives, and claim strategy clearly from the beginning. The more informed homeowners become, the stronger position they place themselves in during the insurance process. And after a serious South Texas hailstorm, that knowledge can make an enormous financial difference.

FAQs

A public adjuster represents the homeowner, while an insurance adjuster represents the insurance company during the claim process.

It depends on the complexity of the claim. Large losses, denied claims, or underpaid settlements often benefit from professional representation.

Yes, in some situations a public adjuster can help reopen or supplement a denied hail claim with stronger documentation and evidence.

Not necessarily, but their responsibility is to evaluate claims for the insurance carrier rather than advocate for the policyholder.

Most public adjusters work on a contingency fee, meaning they receive a percentage of the claim settlement.

Flashing, underlayment, ventilation components, gutters, and soft metal damage are commonly overlooked during initial inspections.

No. Roofing contractors cannot legally negotiate insurance settlements on behalf of homeowners in Texas unless properly licensed.

Simple claims may resolve in weeks, while disputed or supplemental claims can take several months.

Document damage with photos, prevent further property damage if possible, and schedule a professional inspection quickly.

Additional damage is often discovered after repairs begin, especially on roofing systems where hidden issues are not visible during the first inspection.