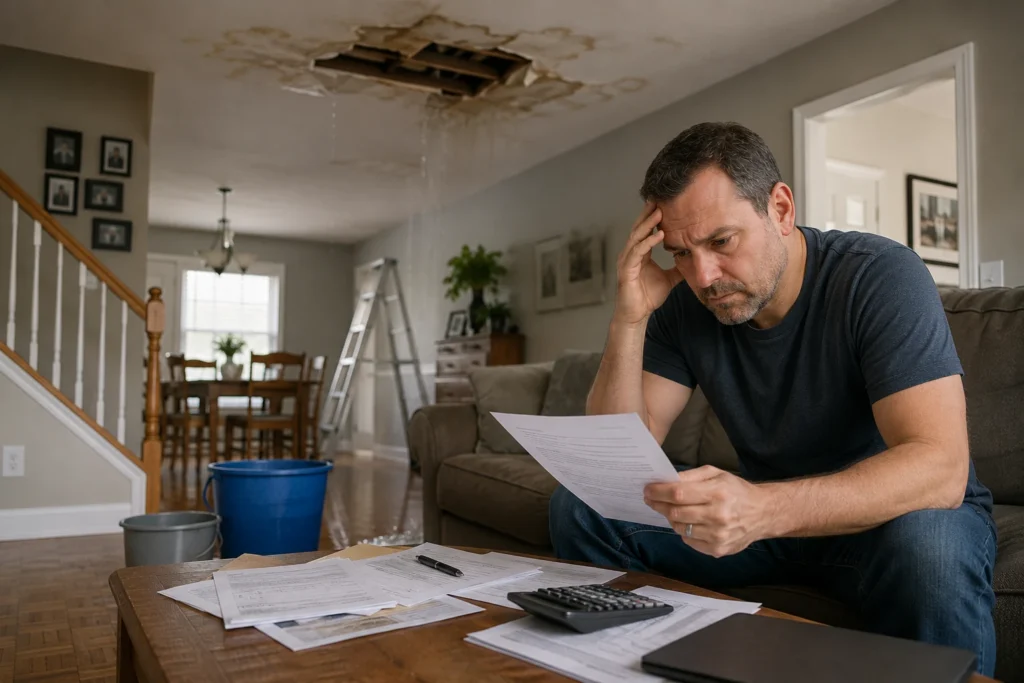

A denied roof claim can feel like a punch to the gut. Especially after a major hailstorm tears through your neighborhood, leaves visible roof damage behind, and suddenly your insurance company says the loss is not covered. Unfortunately, this situation is becoming more common across Texas. And homeowners searching for answers about What to Do If Your Hail Claim Was Denied in Laredo, TX are usually dealing with more than paperwork. They are dealing with stress, leaks, contractor estimates, mounting frustration, and the fear of paying for expensive repairs alone.

I have seen it happen repeatedly. A homeowner files a hail claim expecting help. The carrier inspects the roof quickly. Days later, a denial letter arrives claiming the damage is “wear and tear,” “old deterioration,” or somehow unrelated to the storm that just hit the property.

That does not always mean the claim is over. Far from it. Many denied hail claims are later reopened, supplemented, negotiated, or even reversed entirely when stronger evidence enters the picture. The key is understanding how the process works and responding strategically instead of emotionally. And yes, strategy matters. Especially in Texas.

Why Hail Damage Claims Get Denied in Texas

Insurance carriers rarely describe denials as simple refusals. Instead, they rely on technical explanations, policy language, inspection findings, or coverage limitations to justify the decision. Some denials are legitimate. Others are highly questionable. The challenge is knowing the difference.

Insurance Companies Often Dispute the Cause of Damage

This is one of the most common denial tactics. The carrier may acknowledge roof damage exists while arguing the condition came from:

- Aging

- Thermal cracking

- Foot traffic

- Manufacturing defects

- Poor installation

- Normal wear and tear

That distinction matters enormously because insurance policies generally cover sudden storm damage, not gradual deterioration. Here is the problem though. Hail damage and aging damage can overlap visually. And if the inspection is rushed or incomplete, legitimate storm impacts may get labeled incorrectly. That happens more often than homeowners realize.

Insufficient Documentation

Weak evidence weakens claims. Simple as that. If the file lacks strong documentation, insurers gain leverage quickly.

Common documentation problems include:

- Blurry photos

- No close-up impact images

- Missing weather records

- No contractor inspection report

- No interior moisture documentation

- Missing maintenance history

The stronger your evidence package becomes, the harder it is for a carrier to dismiss the loss casually.

Late Filing Problems

Time hurts hail claims. Sun exposure changes roofing materials. Wind scatters debris. Rain alters interior leak patterns. Temporary repairs erase visible impact marks. The longer a homeowner waits, the easier it becomes for an insurer to argue the damage is unrelated to the reported storm. That timing issue alone destroys many otherwise valid claims.

Deductible and Coverage Disputes

Sometimes the carrier does not fully deny the claim. Instead, they estimate damage below the deductible. Other times they invoke policy limitations such as:

- Cosmetic damage exclusions

- Actual cash value roof endorsements

- Wind/hail percentage deductibles

- Roof age limitations

Texas policies vary widely. Two neighbors with identical roof damage can receive dramatically different outcomes depending on policy structure.

Concurrent Damage Arguments

This gets complicated fast. The insurer may argue multiple factors contributed to the roof condition. Maybe hail impacted the roof, but aging also played a role. Maybe installation defects existed before the storm. These mixed-cause arguments become powerful defense tools for insurance companies because they muddy the claim investigation. And confusion often benefits the carrier.

First Thing to Do After a Hail Claim Denial

Do not panic. Seriously. Many homeowners make expensive mistakes immediately after denial because they assume the decision is final. It usually is not.

Read the Denial Letter Carefully

Most people skim it emotionally. Bad idea. Slow down and study the exact language.

Look for:

- Specific denial reasons

- Policy provisions cited

- Coverage exclusions

- Inspection conclusions

- Dates and timelines

- References to engineering reports

The denial letter tells you exactly where the dispute lives. That matters strategically.

Request the Entire Claim File

This is critical. You want everything connected to the investigation.

Request:

- Adjuster photographs

- Roof diagrams

- Internal estimates

- Engineering reports

- Claim notes

- Inspection summaries

- Recorded statements

You may discover major gaps in the investigation. I have seen denied claims where adjusters photographed only one roof slope. Others ignored soft metals entirely. Some inspections lasted under fifteen minutes. That is not always enough for a reliable hail assessment.

Avoid Immediate Permanent Repairs

Protect the property. Absolutely. But avoid major permanent replacement work before fully documenting the damage whenever possible. Why? Because once the roof changes, proving original storm conditions becomes much harder. Temporary mitigation is usually safer initially.

Examples include:

- Tarping

- Leak stabilization

- Emergency sealing

- Moisture control

Protect the structure while preserving evidence. That balance matters.

Review Your Insurance Policy Like a Professional

Most homeowners never fully read their policy until a claim gets denied. Unfortunately, by then emotions are already high. Still, understanding your policy changes everything.

Understand Your Coverage Type

There is a huge difference between replacement cost and actual cash value coverage.

| Coverage Type | What It Means |

| Replacement Cost | Pays for full replacement minus deductible |

| Actual Cash Value | Deducts depreciation based on roof age |

Older roofs under ACV policies often produce disappointing settlements even when coverage exists. That financial gap surprises many homeowners.

Review Wind and Hail Endorsements

Texas carriers increasingly modify roof coverage through endorsements.

Some policies limit payment for:

- Cosmetic metal damage

- Older roofing systems

- Certain shingle types

- Partial roof replacement

- Matching issues

Read these sections carefully. They often control the entire dispute.

Understand Your Responsibilities After Loss

Policies usually require homeowners to:

- Promptly report damage

- Prevent further deterioration

- Cooperate with inspections

- Preserve evidence

- Submit requested documentation

Failure to meet those obligations can complicate disputes later.

How to Strengthen a Denied Hail Claim

This is where strategy begins shifting. The goal now is not frustration. It is evidence. Strong evidence changes claim outcomes constantly.

Gather Better Photo Documentation

Good roof photos tell a story. Bad photos create confusion. You need both wide-angle and close-up images showing:

- Hail impact marks

- Granule loss

- Bruising

- Cracked shingles

- Damaged vents

- Dented gutters

- Interior staining

Consistency matters too. Photograph the entire roof system, not isolated spots. Homeowners researching How to Document Hail Damage for an Insurance Claim should focus on building organized evidence immediately after the storm. Clear roof photos, timestamped videos, contractor inspection reports, weather records, and written repair estimates all help create a stronger foundation if the insurance company later disputes or denies the claim.

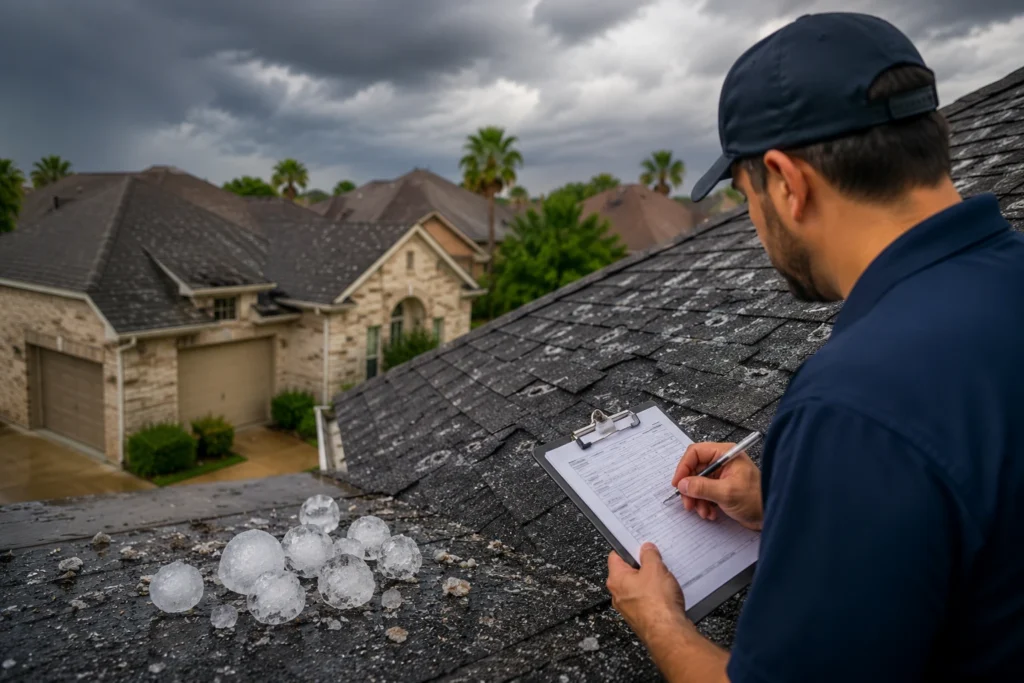

Obtain Independent Roof Inspections

Independent evaluations often uncover damage insurers overlooked or minimized.

Consider obtaining:

- Roofing contractor reports

- Drone imagery

- Moisture scans

- Engineering evaluations

Professional inspections should include detailed written findings, not vague opinions. That documentation carries weight during disputes. Accurate inspections often depend on more than surface-level observations. Some roofing professionals now use advanced imaging tools and moisture-detection methods influenced by broader fields like interferometry, especially when identifying subtle structural inconsistencies after severe hailstorms. Better inspection precision can strengthen disputed roof claims significantly.

Collect Reliable Weather Data

Weather evidence matters enormously in Texas hail claims. Helpful sources include:

- NOAA storm records

- Local radar data

- Hail tracking reports

- Storm verification maps

This helps establish:

- Storm timing

- Hail size

- Wind severity

- Damage consistency

If neighboring properties sustained confirmed hail damage during the same event, that context can strengthen your position.

Build a Detailed Damage Timeline

Chronology matters. Create a timeline showing:

| Event | Date |

| Storm occurrence | Example date |

| First noticed damage | Example date |

| Temporary repairs | Example date |

| Initial inspection | Example date |

| Claim submission | Example date |

| Denial received | Example date |

Clear timelines improve credibility. And credibility matters during negotiations.

Common Insurance Company Tactics After a Denial

Not every insurer behaves unfairly. But certain claim patterns appear repeatedly. Especially after widespread Texas hailstorms.

Blaming Roof Aging

This is extremely common.

The carrier may argue:

- Granule loss came from aging

- Cracks resulted from heat expansion

- Shingle deterioration existed before the storm

Sometimes true. Sometimes not. Independent inspection becomes critical here.

Claiming Mechanical Damage

Insurers occasionally argue roof marks came from:

- Foot traffic

- Maintenance activity

- Tools

- Satellite installation

- Tree contact

Again, context matters. Real hail impacts usually display identifiable characteristics across multiple roof components.

Performing Incomplete Inspections

Short inspections create big problems.

Some adjusters:

- Skip steep slopes

- Ignore detached structures

- Miss soft metal indicators

- Fail to inspect interior leaks

- Avoid attic moisture review

A rushed inspection increases denial risk significantly.

Delaying Communication

Delays wear homeowners down emotionally. That pressure sometimes pushes people into accepting weak settlements or abandoning disputes entirely. Keep records of every communication. Every email. Every phone call. Every inspection date. Organization creates leverage.

Requesting a Reinspection After a Denied Claim

Many denied claims deserve another inspection. Especially when new evidence emerges.

When a Reinspection Makes Sense

Request reconsideration if you now have:

- Better photos

- Contractor reports

- Engineering findings

- Weather verification

- Additional leak evidence

New evidence changes claim dynamics quickly.

What New Evidence Should Be Submitted

Do not resubmit the exact same information. Strengthen the file strategically.

Focus on:

- Clear impact documentation

- Consistent damage patterns

- Independent evaluations

- Detailed roof measurements

- Moisture findings

- Repair estimates

Professional presentation matters too. Organized files are harder to dismiss casually.

Why Contractor Presence Matters

Roofing contractors often identify damage adjusters miss. Having a knowledgeable contractor present during reinspection can improve inspection quality substantially. Not because they argue emotionally. Because they understand roofing systems intimately. That technical perspective matters.

Mistakes Homeowners Make During Reinspections

Avoid these mistakes:

- Becoming confrontational

- Providing inconsistent timelines

- Guessing about technical damage

- Overstating loss severity

- Failing to organize evidence

Calm, organized, evidence-based communication usually performs best.

Understanding the Texas Insurance Appraisal Process

Appraisal is one of the most misunderstood parts of Texas insurance disputes. And one of the most powerful.

What the Appraisal Clause Does

Appraisal helps resolve disagreements involving:

- Repair scope

- Damage valuation

- Amount of loss

It is not a courtroom. It is a dispute resolution mechanism built into many policies.

What Appraisal Cannot Resolve

Important distinction here. Appraisal generally cannot decide:

- Coverage disputes

- Fraud allegations

- Policy interpretation issues

If the insurer completely denies coverage, appraisal may not always solve the problem directly.

How the Appraisal Process Works

The process usually involves:

- Each side selects an appraiser

- Appraisers attempt agreement

- An umpire resolves unresolved differences

- Final award becomes binding

The structure sounds simple. Reality can become highly technical.

When Appraisal Makes Sense for Hail Claims

Appraisal often becomes valuable when:

- Damage was underpaid

- Scope was minimized

- Repairs were omitted

- Partial denials occurred

It is especially effective in valuation disputes.

Costs and Risks of Appraisal

There are costs involved. Potential expenses include:

- Appraiser fees

- Engineering evaluations

- Umpire costs

Timing also matters strategically. Appraisal is powerful, but it is not automatically the right move for every denied hail claim.

Filing a Complaint With the Texas Department of Insurance

Regulatory complaints sometimes help. Sometimes they do not. Still, they can create additional pressure when insurers mishandle claims improperly.

When Filing a Complaint Makes Sense

Consider filing when you believe the insurer:

- Ignored evidence

- Delayed excessively

- Misrepresented policy terms

- Failed to communicate properly

- Conducted inadequate inspections

Evidence That Strengthens a Complaint

Strong complaints rely on documentation.

Helpful materials include:

- Denial letters

- Inspection reports

- Communication logs

- Contractor evaluations

- Timeline summaries

Specific facts matter more than emotional frustration.

What the Texas Department of Insurance Can Actually Do

TDI does not force every claim payment automatically.

But they can:

- Review complaint handling

- Request carrier responses

- Monitor claim conduct

- Investigate regulatory concerns

That oversight sometimes influences claim behavior.

When to Hire a Public Adjuster in Laredo

Some disputes become too complex for homeowners to manage alone. Especially large roof losses.

What a Public Adjuster Does

A public adjuster works for the policyholder, not the insurance company.

Responsibilities may include:

- Reviewing policy language

- Documenting damage

- Preparing estimates

- Organizing evidence

- Negotiating settlements

- Managing claim communications

That advocacy changes claim dynamics significantly.

Signs You Need Professional Help

You may benefit from professional assistance if:

- The claim was denied unfairly

- Large roof replacement costs exist

- Multiple structures were damaged

- Communication stalled

- The insurer keeps changing explanations

Complicated claims require strategy. Not guesswork.

Public Adjuster vs Insurance Company Adjuster

| Feature | Insurance Company Adjuster | Public Adjuster |

| Works For | Insurance company | Homeowner |

| Goal | Control claim exposure | Maximize legitimate settlement |

| Inspection Focus | Carrier perspective | Policyholder perspective |

| Negotiation Role | Company representative | Claim advocate |

That difference matters enormously during disputes.

Why Local Experience Matters in Laredo

Local claim experience creates advantages.

Professionals familiar with Laredo understand:

- Regional storm behavior

- Roofing material patterns

- Texas claim procedures

- Local contractor pricing

- Carrier trends in the area

That regional knowledge helps build stronger claims.

When Legal Action May Become Necessary

Most claims settle without lawsuits. But not all.

Bad Faith Insurance Practices

Texas law requires insurers to handle claims fairly. Potential bad faith behaviors include:

- Unreasonable delays

- Misrepresentation

- Failure to investigate properly

- Unjustified denial patterns

These situations sometimes justify legal review.

Wrongful Denial Situations

Some denials simply do not align with evidence.

Especially when:

- Multiple neighboring homes received approvals

- Storm evidence is overwhelming

- Independent experts confirm damage

Wrongful denial disputes often escalate further.

Important Texas Claim Deadlines

Deadlines matter. A lot. Waiting too long to challenge claim decisions can limit legal options later. Track every important date carefully.

Mistakes That Can Hurt Your Denied Hail Claim

Small mistakes create large problems surprisingly fast.

Throwing Away Damaged Materials

Preserve damaged roofing materials whenever possible. Physical evidence matters.

Repairing Too Much Too Early

Emergency stabilization is smart. Full replacement before documentation? Risky.

Missing Deadlines

Deadlines exist everywhere in insurance disputes. Miss enough of them and leverage disappears quickly.

Relying on Verbal Conversations

Document everything in writing. Always. Phone conversations alone create dangerous ambiguity later.

Failing to Organize Evidence

Disorganized files weaken credibility.

Strong claims usually involve:

- Organized photos

- Written timelines

- Inspection records

- Communication logs

- Weather evidence

Preparation changes outcomes.

How to Protect Future Hail Claims

Prevention helps enormously. Not just physically. Strategically too.

Schedule Annual Roof Inspections

Routine inspections establish roof condition before storms occur. That historical documentation becomes valuable later.

Maintain Organized Property Records

Keep:

- Repair invoices

- Roof warranties

- Inspection reports

- Maintenance records

- Storm documentation

Good records reduce dispute opportunities.

Upgrade Impact-Resistant Roofing Materials

Some roofing systems perform far better during Texas hailstorms. Impact-resistant products may reduce future damage severity substantially.

Review Insurance Policies Annually

Policies change constantly. Coverage reductions often slip into renewals quietly.

Review:

- Deductibles

- Exclusions

- Roof endorsements

- Settlement methods

Before storm season. Not after.

Real-World Problems Homeowners Face After a Hail Claim Denial

The emotional side of a denied hail claim is something insurance companies rarely talk about. But homeowners feel it immediately. A roof claim denial does not arrive in isolation. It usually appears while people are already dealing with stress from storms, leaks, contractor visits, scheduling problems, and financial uncertainty. That pressure builds fast. I have seen homeowners delay repairs because they were unsure what to do next. Others paid for temporary fixes out of pocket while waiting for reconsideration. Some accepted low settlements simply because they felt exhausted by the process.

That is exactly why understanding What to Do If Your Hail Claim Was Denied in Laredo, TX matters so much. A denial creates confusion. But confusion should not control the next decision. One major issue involves hidden roof damage. Not all hail damage creates immediate leaks. Some impacts weaken shingles gradually. Protective granules loosen over time. Small fractures expand under Texas heat. Months later, water intrusion suddenly appears and homeowners wonder why the roof continues deteriorating after the storm. By then, insurers sometimes argue the homeowner waited too long. That creates another dispute entirely.

This is why independent inspections matter even when the roof appears “mostly fine” after a storm. Surface appearance alone does not always tell the full story. Experienced roofing professionals often inspect:

- Soft metal impacts

- Vent damage

- Shingle bruising

- Flashing separation

- Underlayment vulnerabilities

- Moisture penetration points

Those details can dramatically change the strength of a claim. Another common issue involves partial approvals. Sometimes the insurance company approves only minimal repairs while denying full replacement. Homeowners then face a difficult situation. Contractors may explain the roof cannot realistically be repaired section by section due to matching issues, discontinued materials, or widespread impact patterns.

The insurer, however, may still push for spot repairs only. This creates tension quickly. Especially when homeowners are trying to protect long-term property value. In Laredo, roof systems experience intense sun exposure, seasonal storms, heat cycling, and high thermal stress throughout the year. Those conditions accelerate deterioration after hail impacts occur. Even moderate storm damage can worsen much faster under South Texas weather conditions. And that timing matters.

A roof that appears repairable immediately after a storm may deteriorate significantly months later if hidden compromise exists underneath the surface. This is another reason documentation should happen early and thoroughly.

The strongest denied hail claims often share similar characteristics:

| Strong Claim Characteristics | Why They Matter |

| Detailed roof photos | Creates visual evidence |

| Independent inspections | Adds technical credibility |

| Organized communication records | Prevents timeline disputes |

| Verified storm reports | Supports causation |

| Consistent documentation | Strengthens reliability |

| Fast mitigation efforts | Shows responsible ownership |

Weak claims usually show the opposite pattern. Missing records. Poor photos. Delayed reporting. Inconsistent timelines. Insurance companies notice those weaknesses immediately.

That does not mean homeowners are dishonest. Most simply are not prepared for how technical hail disputes become once denial enters the process. Roofing systems, policy endorsements, depreciation calculations, engineering opinions, weather analysis, and settlement procedures suddenly collide all at once. It becomes overwhelming. That is why calm organization matters more than emotional reactions.

Every document should support the same overall narrative:

- A storm occurred

- Damage resulted

- The loss was documented

- The homeowner acted responsibly

- The insurer overlooked, underestimated, or disputed legitimate damage

Consistency builds credibility. And credibility drives negotiations. Homeowners should also understand one important reality about denied hail claims in Texas. Many disputes eventually settle after additional evidence appears. Not because the storm damage suddenly changed.

Because the documentation improved. That distinction matters enormously. Insurance carriers often make decisions based on the information available during the initial inspection. If the first inspection was rushed, incomplete, or poorly documented, the resulting denial may reflect limited evidence rather than the full condition of the property.

This is especially important for homeowners researching What to Do If Your Hail Claim Was Denied in Laredo, TX after receiving frustrating inspection results. A denial can sometimes become the beginning of a stronger second investigation instead of the end of the claim. And that shift in mindset changes everything.

Why Denied Hail Claims Are Often Reopened Successfully

A denial is not always the end. Far from it. Many homeowners recover substantial settlements after initially denied claims because stronger evidence eventually enters the process. Independent inspections uncover missed impacts. Weather data strengthens storm correlation.

Detailed timelines improve credibility. Professional representation changes negotiation dynamics. Persistence matters too. Insurance disputes are often evidence battles, not emotional battles. And the homeowner with the strongest documentation usually stands in the strongest position.

If you are dealing with What to Do If Your Hail Claim Was Denied in Laredo, TX, focus on strategy first. Organize your evidence. Understand your policy. Strengthen your documentation. Seek professional guidance when necessary. Most importantly, do not assume the first answer is the final answer. Because in Texas hail claims, it often is not.

FAQs

Yes. Many denied hail claims are reopened after homeowners submit stronger documentation, inspection reports, or additional storm evidence.

Deadlines vary by policy, but acting quickly is important because delays can weaken evidence and legal options.

Independent roof inspections and weather documentation can help prove the damage came from a recent hailstorm rather than normal aging.

Absolutely. A second inspection often uncovers damage the original adjuster missed or underestimated.

Yes. Hail impacts can weaken roofing materials and eventually lead to leaks, moisture intrusion, and structural deterioration.

Photos, contractor reports, weather records, repair invoices, inspection summaries, and written communication logs all help.

It can. Appraisal is commonly used when homeowners and insurers disagree on repair scope or claim value.

A public adjuster may help if the claim is complex, underpaid, delayed, or denied unfairly.

Yes. Homeowners can submit complaints to the Texas Department of Insurance if they believe the claim was mishandled.

Avoid throwing away damaged materials, missing deadlines, or making major repairs before fully documenting the damage.